Let me ask you something that sounds simple but opens up a rabbit hole most people never expect.

If someone handed you $1,900 in the year 1900, what would that actually mean in today’s money? The answer isn’t just surprising — it’s borderline shocking. And once you understand it, the way you look at historical prices, wages, and wealth will never quite be the same.

Let’s dig in.

The Number First — Then the Story Behind It

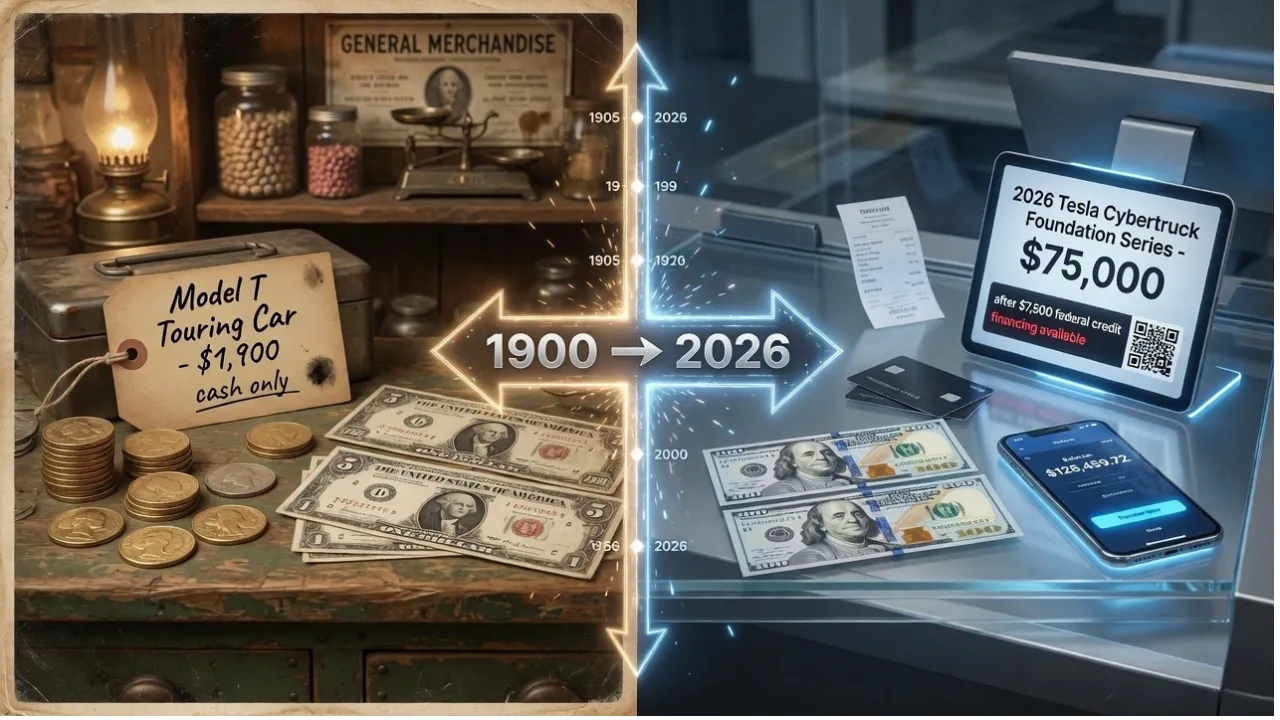

By most reliable inflation calculators, using the U.S. Consumer Price Index (CPI) as the benchmark, $1,900 in 1900 is roughly equivalent to $73,000 to $78,000 in 2026. Some calculations, depending on the methodology used, push that figure even higher — closer to $85,000 when accounting for certain economic factors like purchasing power parity and wage-based inflation models.

That’s not a typo. Nineteen hundred dollars in 1900 buys you what roughly seventy-five thousand dollars buys today.

And if that number doesn’t hit you immediately, sit with it for a moment. Because here’s the thing — that’s not magic. That’s a century and a quarter of inflation, compounding steadily, reshaping the value of every dollar that ever existed.

What Was Life Like in 1900?

To really grasp the weight of $1,900 back then, you need to picture the world as it was.

In 1900, the average American worker — a factory hand, a clerk, a farm laborer — earned somewhere between $400 and $500 per year. A skilled tradesman, say a carpenter or a machinist, might pull in $600 to $800 annually if things were going well. Doctors, lawyers, and engineers were doing considerably better, but even they rarely cracked $2,000 in a single year.

So $1,900 in 1900 wasn’t just “decent money.” It was, for most working-class Americans, nearly four years’ worth of wages. Four years. That puts $1,900 somewhere in the territory of serious wealth — not robber-baron rich, but absolutely, genuinely comfortable by any standard of the era.

You could buy a modest house in a mid-sized American city for $1,500 to $2,500. A brand-new Ford Model T — when it arrived in 1908 — would set you back $850. A pound of steak cost roughly 14 cents. A dozen eggs? About 21 cents. A full week’s worth of groceries for a family of four could be handled for under $5.

That was the world $1,900 lived in.

How Inflation Actually Works — And Why It Matters

Most people think of inflation as a recent problem. Turn on the news in any given year and someone is complaining that prices are going up. But inflation isn’t new. It’s been the persistent, background hum of every modern economy for well over a century.

The United States has averaged roughly 3.2% to 3.5% inflation annually since 1900. That doesn’t sound dramatic until you run the math over 126 years. Compound anything for long enough, and the results become almost surreal.

Here’s the simple version: every 20 to 25 years or so, prices roughly double. That means money sitting still loses half its purchasing power in just a couple of decades. Over 126 years, we’re looking at six or seven of those doublings — which is exactly how $1,900 becomes $75,000.

The major inflationary periods that drove this transformation weren’t random. World War I sent prices soaring. The Great Depression created a brief deflationary dip, but World War II reignited price pressure sharply. The 1970s oil crisis brought what economists call “stagflation” — inflation without economic growth — and average prices doubled in under a decade. The post-COVID period of 2021 to 2023 added another jolt, with inflation hitting peaks not seen since the early 1980s.

Each of those episodes chipped away at the dollar’s purchasing power. And over 126 years, all those chips add up to something enormous.

The Psychological Trap of Nominal Numbers

Here’s where it gets philosophically interesting.

We’re wired to think about money in terms of the number printed on the bill or the balance shown on the screen. $1,900 looks like $1,900. It always will. But the number itself is almost meaningless without context — without knowing what year we’re in and what that money can actually buy.

Historians sometimes make this mistake when they talk about historical wealth or salaries. They’ll report that someone earned “$500 a year in 1890” without flagging that this was a solid middle-class income. Or they’ll note that a famous painting sold for “$50,000 in 1950” without pointing out that this would be the equivalent of well over half a million dollars today.

This is why financial literacy — real financial literacy, not just knowing how to balance a checkbook — includes understanding purchasing power. It includes understanding that a dollar is a unit of account that changes meaning over time, not a fixed measure of value.

Gold investors, real estate enthusiasts, and seasoned economists have understood this for decades. The rest of us are catching up slowly.

What Would $1,900 Today Actually Buy?

Fast-forward to 2026. You’re holding $1,900. What does it mean now?

It’s a decent month’s rent in a smaller American city, maybe a bit more. It’s a round-trip international flight with some spending money left over. It covers roughly two to three months of groceries for a family. It’s a used car with high mileage and no warranty. It’s a starting point — useful, but not transformative.

Now compare that to what $1,900 could have done in 1900: buy you a house. Fund your family for four years. Set you up in a small business. That gap — that gulf — between what those dollars represent is the story of 126 years of inflation.

The Takeaway

Money is time. Money is history. Money is context.

The next time you read about what something cost a hundred years ago, resist the temptation to think “that was so cheap!” It wasn’t cheap. It was priced for a world where a dollar had the muscle that many dozens of today’s dollars now carry.

$1,900 in 1900 wasn’t a number. It was a life-changing sum for most Americans. In 2026, it’s a good start on next month’s bills.

And that, more than anything, is what inflation really means.